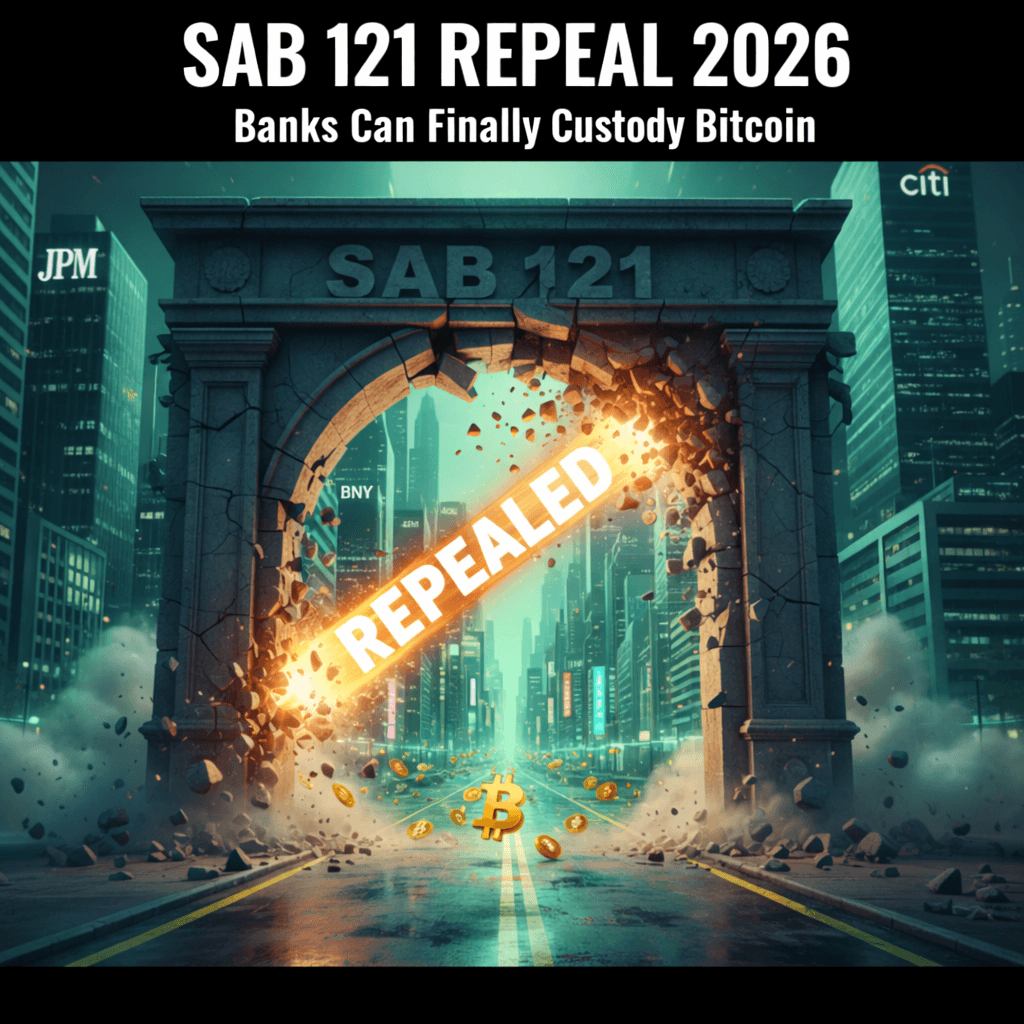

The SAB 121 repeal 2026 marks a historic turning point for the American financial landscape, as the SEC officially moves from “Enforcement to Endorsement.” For years, a single paragraph of accounting guidance acted as a “keep out” sign for America’s largest banks; Staff Accounting Bulletin 121 (SAB 121), issued in 2022, essentially made it financially impossible for traditional banks to hold Bitcoin for their customers.

Following President Trump’s January 2025 Executive Order, the SEC staff rescinded the controversial bulletin and replaced it with SAB 122. As we move through February 2026, the results are clear: the floodgates for institutional bank custody have finally opened.

- The Crypto Native: Companies like Coinbase have the best tech but are still relatively new in the eyes of traditional finance.

- The Legacy Giant: Banks like BNY Mellon (the world’s largest custodian) now offer Bitcoin storage backed by centuries of trust and “Bank-Grade” insurance.

This creates what we call “Safety Arbitrage.” While an exchange might offer more trading features, a bank offers a level of regulatory protection that is attractive to “high-net-worth” individuals and pension funds.

Is your Bitcoin safer in a bank? Use our Asset ROI Comparison Tool to see the fee differences and insurance levels between traditional bank custody and crypto-native platforms.

How the Repeal Impacts Bitcoin’s Price Stability

One of the biggest reasons for Bitcoin’s volatility in the past was the “Concentration Risk.” Because only a few companies could hold large amounts of BTC, any issue with one company (like the FTX collapse) sent shockwaves through the market. (Check Top 3 Self Custody Wallets for 2026)

With the SAB 121 Repeal 2026, Bitcoin is being distributed across thousands of regulated banks. This “Democratization of Custody” makes the network much more resilient. It also allows Bitcoin to finally behave like “Digital Gold” an asset that institutions can hold on their balance sheets without fear of a regulatory ambush.

The Bottom Line: A “Green Light” for the Midterms

As we approach the 2026 midterms, the repeal of SAB 121 stands as one of the most significant wins for the “Crypto EO” (Executive Order). It signals that the US government is no longer trying to “unbank” the crypto industry, but is instead trying to “onboard” it.

Whether you prefer self-custody or the security of a global bank, one thing is certain: the “Accounting War” on crypto is over.